PHI TRENDS: HERE’S WHAT INVESTORS CAN ANTICIPATE FOR THE REST OF 2021

2020 has clearly depicted that investors must focus on prioritising companies with sound business models, writes entrepreneur and investor Shailesh Dash

The year gone by, 2020, was primarily overshadowed by the Covid-19 pandemic. Thankfully, a lot has changed now, with light at the end of the tunnel thanks to vaccine rollouts and the reopening of economies.

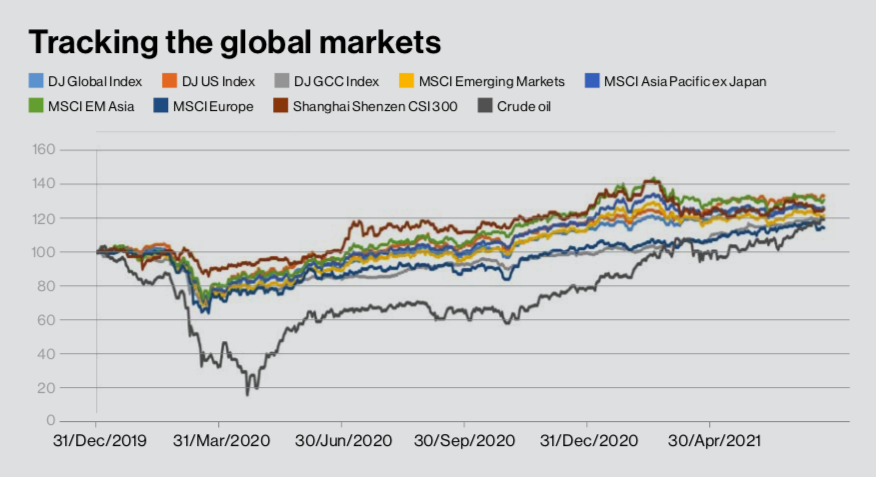

The fall in equity markets started in late February 2020, and continued into most of March 2020 before rallying strongly in the subsequent months. After a strong performance witnessed in 2020, the year 2021 started with renewed bouts of volatility, especially concerns over slow vaccine rollouts, new waves of virus in some countries and delays in fiscal support from the US Fed. The performance during the first part of 2021 (until May 23, 2021) was largely supported by encouraging economic indicators and robust earnings during the first quarter.

The Dow Jones Global Index appreciated by 10.8 per cent this year (as of May 23), after rising by 14.1 per cent in 2020. While the Dow Jones US index rose by 12.9 per cent this year compared to 18.3 per cent in 2020, the European markets were up by 11 per cent compared to gains of 3.1 per cent in 2020. For the emerging economies, equity markets are experiencing pull-backs after recording strong gains in 2020, which can be attributed to policy tightening by China and virus-led restrictions impacting growth in certain parts of the region.

GCC equity markets are witnessing strong performance with gains of 21.1 per cent in 2021 (as of May 23) after declining by 0.9 per cent in 2020. This can be attributed to the roughly 50 per cent rise in oil prices coupled with measures adopted by the regional governments, especially the UAE and Saudi Arabia, to attract investments into the region.

What next?

Investors should clearly understand the divergence in pace of economic recovery around the globe. For instance, the US and China are witnessing a much quicker recovery compared to Europe. The supportive monetary policy by central banks will further boost economic activity.

The extent of economic recovery is likely to deepen and broaden during the next two quarters, crystalising the divergence within the global economies.

There are broadly two concerns clouding the equity markets – inflation and new Covid-19 variants that could lead to short-term volatility in the second half of 2021. Inflation has emerged to become a rising concern, and investors are finding it difficult to interpret its impact on the broader markets because of mixed views from experts and market participants.

There is a growing belief that the inflationary pressure could be transitory and the slack in global economies could reduce the pricing power from companies going forward. This thesis is broadly supported by the fact that the US is operating at below full employment while wage growth is limited.

Another risk to economic recovery is the lingering concerns of Covid-19 variants, which might be resistant to vaccines, coupled with the slow rollout of vaccines in some parts of the world.

Going forward, there is no doubt about the world heading into a full recovery from Covid-19 during the second half of 2021. However, investors must be prepared for higher uncertainty in equity markets, with no meaningful corrections in the near term.

Regardless of the course of the markets, 2020 has clearly depicted that investors must remain focused on prioritising companies with sound business models which have the ability to emerge strong from any crisis or recession.

It is important for investors to understand the changes that are expected to remain and reflect those by rebalancing their portfolios. For example, tech stocks will continue to remain relevant, given their dominant position in the new normal.

Comments